Debt collectors must follow strict rules when trying to collect money. These rules come from the Fair Debt Collection Practices Act (FDCPA), a federal law designed to protect consumers from harassment and deception.

Unfortunately, many collectors still cross the line. Understanding common fdcpa violations helps you protect your rights and take action if a collector behaves unfairly.

In this guide, we’ll break down the most common violations in simple terms so you know exactly what debt collectors can and cannot do.

Table of Contents

Threatening Actions They Cannot Legally Take (FDCPA Violations)

Some collectors attempt to intimidate people into paying by issuing threats they cannot legally carry out. This is one of the most common fdcpa violations.

Examples include:

- Threatening lawsuits without legal authority

- Claiming they will garnish wages immediately

- Saying you will be arrested for unpaid debt

- Threatening property seizure without court action

Collectors can only take actions they are legally allowed to pursue. If they make empty threats or exaggerate consequences, they are violating federal law.

You also have the right to request proof that the debt actually belongs to you. If they cannot verify it, the collection must stop.

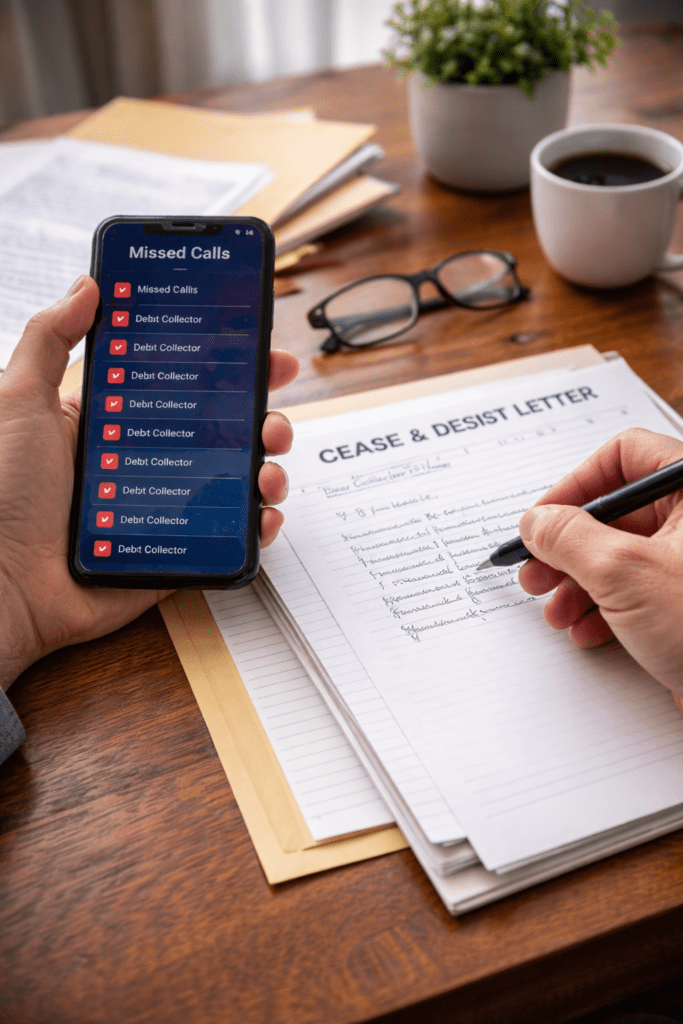

Continuing Contact After You Ask Them to Stop (FDCPA Violations)

Another frequent example of fdcpa violations occurs when collectors keep calling after you ask them to stop.

You are not required to communicate by phone. Once you request written communication only—or send a cease-and-desist letter—the collector must respect that request.

Violations include:

- Repeated daily calls

- Calling after being told to stop

- Contacting you through multiple numbers

- Harassing voicemails

Written communication is safer because it creates proof of what was said. If calls continue after your request, the collector may face legal consequences.

Failing to Identify Themselves as Debt Collectors

Collectors must clearly tell you who they are and why they are calling. This is known in the industry as the required disclosure.

During initial contact, they must explain:

- They are a debt collector

- They are attempting to collect a debt

- Information obtained will be used for collection

If a caller hides their identity or pretends to be someone else, it becomes a violation.

Consumers deserve transparency so they can make informed decisions.

Sharing Your Debt Information with Others

Your debt is private financial information. Collectors cannot discuss it with friends, neighbours, coworkers, or relatives who are not responsible for the debt.

Illegal disclosures include:

- Talking about debt with neighbours

- Calling coworkers repeatedly

- Revealing debt details to family members

- Leaving messages revealing debt information

The only exceptions usually involve your spouse or the legally responsible parties.

Privacy protection is a major part of consumer law.

Lying or Using Deceptive Tactics

Debt collectors cannot lie or mislead you in order to collect money.

Common deceptive practices include:

- Pretending to be attorneys or government officials

- Claiming you committed a crime

- Misstating debt amounts

- Sending fake legal-looking documents

- Threatening actions that cannot legally occur

Collectors must present accurate information at all times. If they misrepresent facts, consumers may be eligible for damages.

Honesty is not optional—it is required by law.

Calling at Inconvenient Hours

Collectors must respect reasonable contact times. Calls before 8 a.m. or after 9 p.m. usually violate federal rules unless you agree otherwise.

Problematic behaviour includes:

- Early morning calls

- Late-night calls

- Calling during known inconvenient times

- Ignoring work-hour restrictions

Debt collection should not disturb your personal or professional life.

If calls occur outside legal hours, keep records of dates and times.

What Should You Do If Your Rights Are Violated?

If you experience unfair treatment:

- Keep records of calls, messages, and letters.

- Request debt validation in writing.

- Send a cease-and-desist letter if needed.

- Consult a consumer protection attorney.

- File complaints with consumer agencies.

Many consumers don’t realise they may be entitled to compensation when collectors break the law.

You May Need More

FAQs

What are the most common FDCPA violations?

Common violations include repeated harassment calls, threats of arrest or lawsuits without legal basis, contacting third parties about your debt, using abusive language, and misrepresenting the debt amount. Federal law requires debt collectors to communicate honestly and respectfully.

When should you report FDCPA violations?

You should report violations as soon as harassment or illegal practices begin. Early reporting helps preserve call logs, letters, and messages, which serve as critical evidence if legal action becomes necessary.

Where can consumers file complaints about debt collector misconduct?

Consumers can submit complaints to federal or state consumer protection agencies or consult consumer rights attorneys. Documentation strengthens complaints and increases the chances of corrective action.

How do FDCPA violations affect consumers financially?

Illegal collection tactics can cause stress, financial pressure, and sometimes wrongful payments on invalid debts. However, consumers may recover damages if collectors violate federal law.

Who oversees debt collection practices?

Debt collection agencies must comply with federal consumer protection laws. Oversight is conducted through federal and state consumer protection authorities that enforce compliance standards.

References

- Fair Debt Collection – National Consumer Law Centre

- Understanding and Following the Fair Debt Collection Practices Act by Michelle Dunn

- Fair Debt Collection Practices Act: Volume 1 – Landmark Publications

- Fair Debt Collection Practices Act: Volume 2 – Landmark Publications

- Fair Debt Collection Practices: Federal and State Law and Regulation (LexisNexis)

- Consumer Protection Law in a Nutshell – Dee Pridgen

- A Guide to Collection Self Defence by Brian Parker

- ACA International’s Guide to the Fair Debt Collection Practices Act

- The Debt Relief Playbook: How to Defeat Creditors and Collectors

- Bad Paper: Chasing Debt from Wall Street to the Underworld by Jake Halpern

Final Verdict

Debt collection is legal—but harassment, deception, and intimidation are not. Understanding common fdcpa violations empowers you to respond confidently and protect your financial and personal well-being.

If collectors break the rules, you don’t have to tolerate it. Know your rights, document everything, and seek help when necessary.

The more informed you are, the easier it becomes to stop unfair collection practices.