Falling behind on debt can feel overwhelming, especially when legal actions begin. One of the most serious collection tools a creditor can use is a bank levy. A bank levy can suddenly freeze your bank account, block access to your money, and disrupt your ability to pay everyday expenses.

Understanding how a bank levy works, what funds are protected, and what steps you can take to stop or reduce its impact can help you regain control before lasting damage is done. This guide explains bank levies in plain language, focusing only on what readers actually need to know to protect themselves.

Table of Contents

What Is a Bank Levy?

A bank levy is a legal process that allows a creditor to take money directly from your bank account to pay an unpaid debt. When a levy is issued, your bank must freeze funds in your account up to the amount owed and eventually send that money to the creditor.

Unlike wage garnishment, where money is taken gradually from each paycheck, a bank levy targets the funds you already have on deposit. This makes it one of the most aggressive debt-collection methods available.

In most situations, a creditor must first sue you and win a court judgment before requesting a bank levy. However, some government agencies have special authority to levy accounts without court approval.

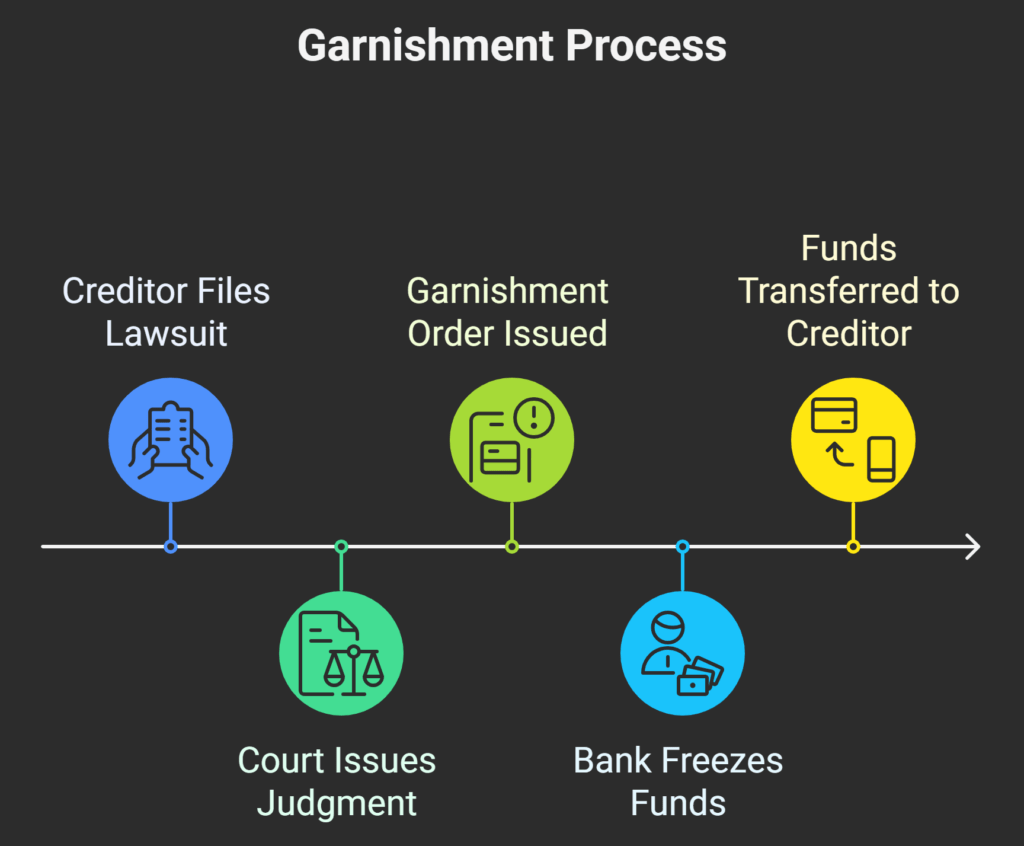

How a Bank Levy Works Step by Step

A bank levy does not happen overnight. There is usually a clear legal process that leads up to it.

1. Collection Attempts Come First

Before seeking a bank levy, creditors typically attempt to collect the debt through calls, letters, payment reminders, or settlement offers. Ignoring these efforts often increases the chance of legal action.

2. Lawsuit and Court Judgment

Most private creditors must file a lawsuit and win a judgment against you. If you do not respond to the lawsuit, the creditor may receive a default judgment, making a bank levy easier to obtain.

Government agencies such as the IRS or state tax authorities can levy accounts without court approval, but they are still required to provide notice in advance.

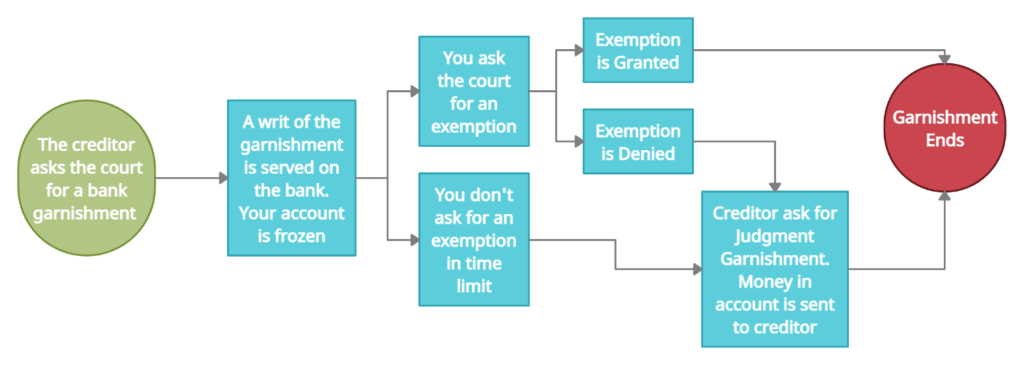

3. Account Freeze and Transfer of Funds

Once the levy is served, your bank freezes the specified amount in your account. During this period:

- You may not access the frozen funds

- Checks and automatic payments may bounce

- Overdraft and bank fees may apply

After a waiting period set by state law, the bank releases the funds to the creditor unless the levy is stopped or challenged.

What Money Is Protected From a Bank Levy?

Not all money in your account can legally be taken through a bank levy. Federal law protects certain types of income, even if they are deposited into your bank account.

Commonly exempt funds include:

- Social Security benefits

- Supplemental Security Income (SSI)

- Veterans benefits

- Federal retirement benefits

- Railroad retirement benefits

- Child support payments

- FEMA disaster assistance

- Certain student loan disbursements

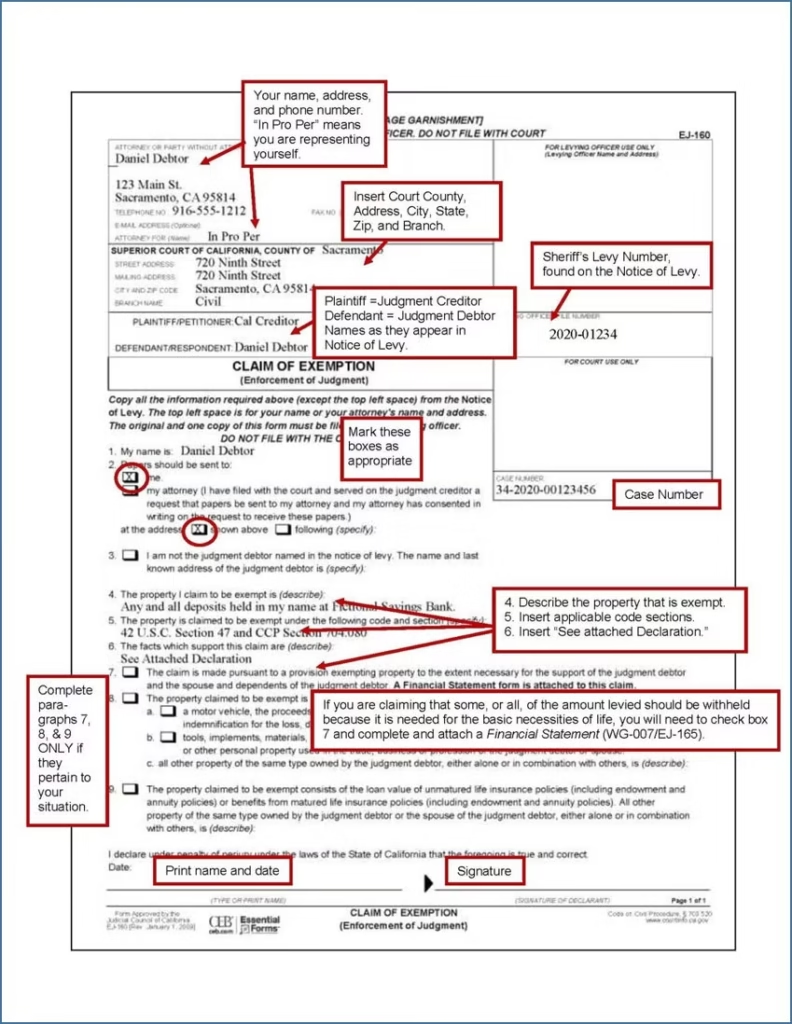

Many states also require creditors to leave a minimum balance in your account so you can meet basic living expenses. The protected amount varies by state.If exempt funds are frozen, you may need to file an exemption claim quickly to have the money released.

You can also go with the National Legal Aid and Defender Association (NLADA) database.

How Long Does a Bank Levy Last?

A bank levy does not follow a single, universal timeline. How long it lasts depends on who the creditor is, what type of debt is involved, and how quickly you take action. For some people, the levy is a one-time freeze. For others, it can continue until the debt is fully paid or legally resolved.

Understanding these timelines can help you decide your next move before more money is taken.

One-Time Bank Levies vs. Ongoing Levies

In many states, a bank levy is a one-time seizure. This means the creditor can only take the money that is in your account at the moment the levy is enforced. Once those funds are transferred, the levy ends—unless the creditor files again.

However, some levies can be repeated or ongoing, especially when:

- The debt is large

- The creditor is a government agency

- State law allows renewed levies

If the judgment remains unpaid, the creditor may issue another levy later, targeting any new funds deposited into your account.

How Long Does the Bank Freeze Your Account?

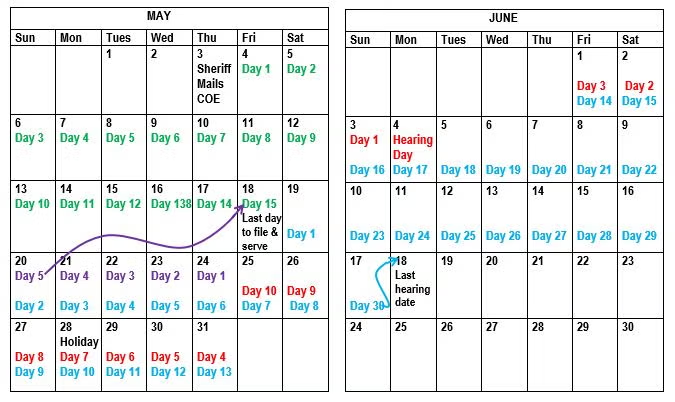

After receiving a bank levy order, your bank typically freezes the funds for a short waiting period, often ranging from 10 to 30 days, depending on state law.

During this time:

- You usually cannot access the frozen money

- Automatic payments and checks may fail

- You may file objections or exemption claims

If no action is taken within this window, the bank releases the money to the creditor.

How Long IRS Bank Levies Last

An IRS bank levy works differently from private creditor levies. The IRS generally freezes your account for 21 days before taking the funds. This waiting period is designed to give you time to:

- Prove financial hardship

- Request a levy release

- Set up a payment plan

If no agreement is reached, the IRS takes the money after the 21-day period. Unlike many private levies, IRS levies may continue until the tax debt is fully resolved.

When a Bank Levy Ends Automatically

A bank levy may end on its own if:

- The debt is paid in full

- The creditor agrees to lift the levy

- The court orders the levy removed

- The statute of limitations expires

- You successfully proved the funds are exempt

Once lifted, the bank must release any remaining frozen funds back to you.

Can a Bank Levy Last for Years?

Yes—indirectly. While a single levy event may be short, a valid judgment can last years (often 5–20 years depending on state law) and may be renewed. As long as the judgment is active, the creditor may continue using collection tools, including repeated bank levies.

This is why early negotiation or legal intervention is critical.

How to Shorten the Duration of a Bank Levy

You may be able to shorten or stop a bank levy by:

- Filing an exemption claim immediately

- Negotiating a settlement or payment plan

- Demonstrating financial hardship

- Challenging improper or expired debts

- Filing for bankruptcy, which usually pauses levies instantly

The sooner you act, the greater your chance of limiting how long the levy affects your finances.

How to Stop or Remove a Bank Levy

Although a bank levy is serious, it is not always permanent. Acting quickly is critical.

Challenge Errors

Mistakes happen. If the debt is not yours, the amount is incorrect, or identity theft is involved, you can challenge the levy in court and request reimbursement of fees.

Claim Exempt Funds

If your account contains protected income, file an exemption claim immediately with the bank or court. Documentation is usually required.

Negotiate With the Creditor

Many creditors prefer voluntary payments over legal enforcement. A payment plan or settlement agreement may convince the creditor to lift the bank levy.

Check the Statute of Limitations

If the debt is legally too old to collect, the levy may be invalid. A consumer law attorney can confirm whether this applies.

Consider Bankruptcy

Filing for bankruptcy triggers an automatic stay, which usually stops bank levies immediately. Bankruptcy does not erase all debts, but it can provide powerful legal protection.

Limit Account Activity

If the levy is ongoing, avoid depositing new funds until the issue is resolved. While this does not stop the levy, it can reduce losses.

Can the IRS Release a Bank Levy?

Yes — the IRS can release a bank levy, but only under specific conditions. If you act quickly and follow the correct steps, you may be able to get your bank account unfrozen and regain access to your money.

However, it’s important to understand one key point: a levy release does not erase your tax debt. It simply stops the immediate collection action while the IRS works with you on a solution.

When the IRS Will Release a Bank Levy

The IRS may release a bank levy if any of the following situations apply:

1. The Levy Is Causing Immediate Financial Hardship

If the levy prevents you from paying for basic living needs — such as rent, food, utilities, or medical care — the IRS may classify this as economic hardship.

You will usually need to show:

- Proof of income and expenses

- Bank statements

- Bills showing essential living costs

If approved, the IRS can release the levy to prevent further harm.

2. You Enter a Payment Plan With the IRS

One of the most common ways to stop an IRS bank levy is by setting up an instalment agreement.

Once a payment plan is approved:

- The IRS may release the levy

- Future levies are usually paused as long as payments are made on time

This option works best if you can afford monthly payments.

3. The Levy Was Issued in Error

Mistakes happen. The IRS may release a levy if:

- The debt was already paid

- The statute of limitations expired

- Proper notice was not given

- The levy targeted the wrong account

If an error is confirmed, the IRS must release the levy promptly.

4. The Debt Is Being Resolved Through Another Method

The IRS may release a bank levy if you qualify for:

- Currently Not Collectable (CNC) status

- Offer in Compromise approval

- Bankruptcy protection

These options signal to the IRS that alternative resolution steps are underway.

How Long Does It Take for the IRS to Release a Levy?

After the IRS agrees to release a bank levy, the release is usually processed within a few days, but banks may take additional time to unfreeze the account.

If timing is critical, contacting your bank directly after approval can help speed up access to your funds.

What the IRS Will NOT Do

The IRS will not automatically release a levy just because:

- You are unhappy with the levy

- You ignore notices

- You plan to deal with it later

Silence almost always leads to the funds being taken.

Other Ways Creditors Can Collect a Judgment

A bank levy is only one method available to judgment creditors.

Wage Garnishment

Creditors may take a portion of your paycheck directly from your employer. Limits apply, and some income is protected.

Property Liens

A lien can be placed on real estate, vehicles, or business assets. This prevents selling or refinancing without paying the debt.

Seizure of Personal Property

In limited cases, creditors may seize valuable non-essential property. Most states protect basic household goods, tools for work, and retirement accounts.

Further readings you may need

Guide to Fair Child Custody Arrangements After Divorce

How To Prove Adultery In Divorce

Wrap up

A bank levy can disrupt your financial life quickly, but it does not mean you are out of options. Understanding how bank levies work, which funds are protected, and how to respond gives you the power to act before permanent damage occurs.

If you receive notice of a lawsuit or levy, do not ignore it. Early action—whether through negotiation, legal advice, or formal exemptions—can protect your money and reduce long-term consequences.

If you are already facing financial hardship, seeking help sooner rather than later can make the difference between recovery and deeper financial stress.